Medicare Supplements – also known as Medigap – have been around for about as long as Medicare has. You probably have asked yourself, What is a Medicare Supplement Plan (Medigap)? Since you have shares of cost with Original Medicare like 20% for most medical services, supplemental policies were created to cover those expenses for you. Many individuals that are “New to Medicare” are surprised to find out how high the Part A deductible is and that Medicare only covers 80% of your Part B expenses. The aim of these plans is to provide peace of mind through predictable, lower shares of cost than what you would experience under Original Medicare.

With a Medicare Supplement Plan, you are getting three things:

- Low to no copays and coinsurances for Medicare services.

- High Monthly Premium.

- No network restrictions.

Enrolling Into A Medicare Supplement Plan

You must have both Part A and Part B to purchase a supplement policy. Medicare Supplement plans will cover only one person, so your spouse must have his or her own individual policy. The good news is many carriers offer household discounts if two or more people enroll in Medicare Supplement plans from the same insurance company.

Upfront the biggest barrier to enrolling into a Medicare Supplement is going to be income. It’s for this reason only 16-18% of all Medicare recipients have chosen a Medicare Supplement plan as their option to manage their Medicare coverage. Monthly Premiums for these plans can range from as low as $40 up to $260 per month for a 65-year-old depending on how much coverage you wish to have. The price considers two main variables:

- How old you are

- How much coverage the plan you purchase will provide

Medicare Supplement Plan Important Note! Many aren’t clear that Medicare Supplement plans can deny you based on your current health and health history.

Generally, when you apply for a Medicare Supplement you will have to answer a series of questions about your health history and medications to see if the health plan is willing to accept you. The main exception is when you first enroll into Medicare or when you first get Part B. You will have a short window to enroll into a Medicare Supplement plan with a guarantee to be accepted. This window begins on the first day of your birth month or the month that you enroll in Part B, lasts for six months, and is a “use it or lose it” enrollment period. During this time period, the insurance company cannot ask you any medical questions, they cannot turn you down for any health conditions, and they cannot charge you any additional amount due to health conditions, medications or pre-existing illnesses.

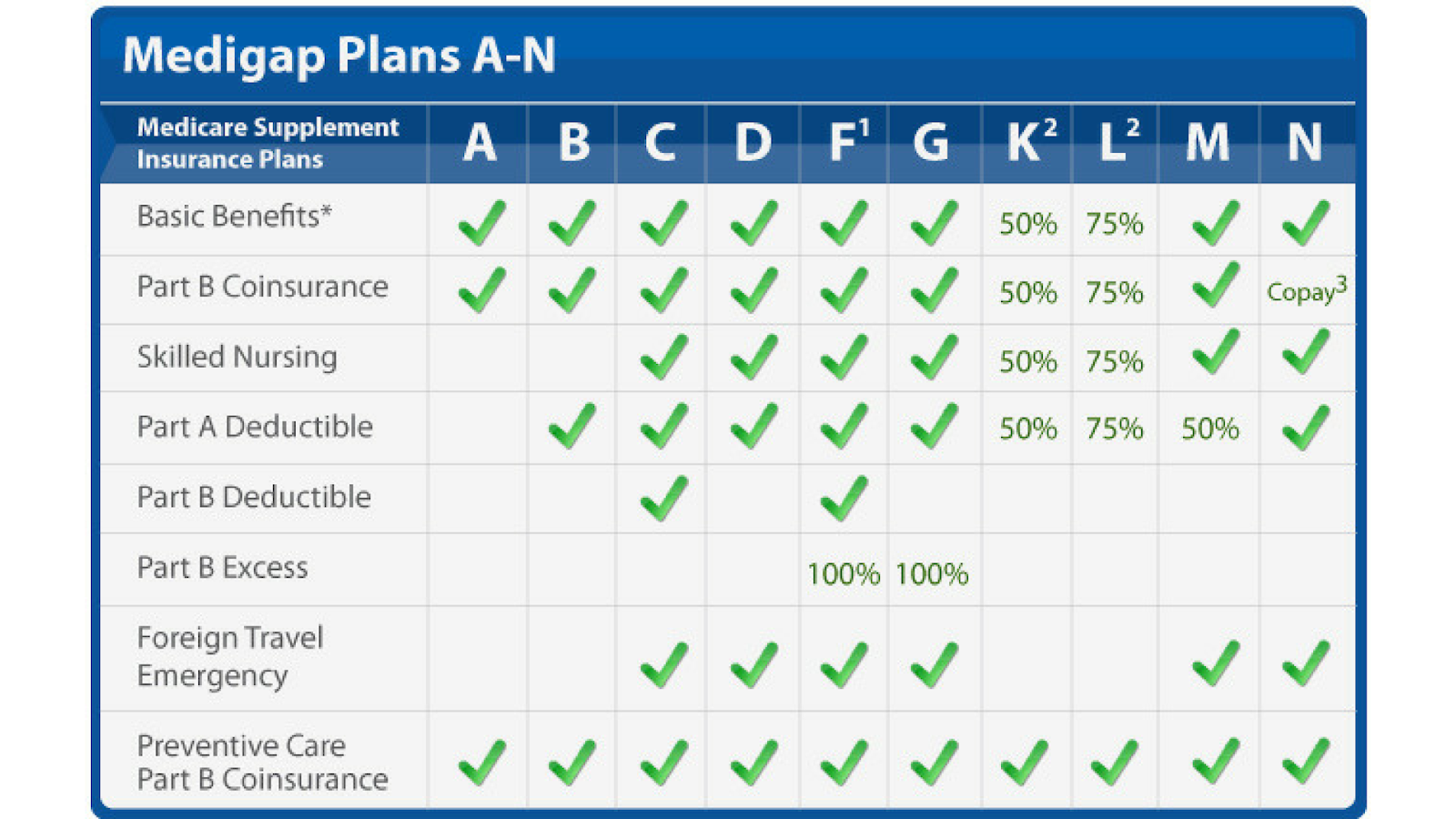

Each private insurance company can choose which plans they are going to offer; however, the plan benefits will be identical to all like plans that other private insurance companies choose to offer as well. For example, you may find Plan F at different companies, but by regulation the coverage of Plan F will be identical at each company. The monthly price of each Plan F is the only thing that may vary. Prices will often be within 5% of each other ($10 per month difference at most). Below is a chart of the various plans a company may offer and the coverage they provide.

All supplement plans are labeled with an alphabetical letter. Be sure not to confuse Plan C with Medicare Part C, which is a completely different package.

Medigap Plan F

*Medigap Plan F is also offered as a high-deductible plan by some insurance companies in some states. If you choose the high-deductible option, it means you must pay for Medicare-covered costs (coinsurance, copayments, deductibles) up to the deductible amount of $2370 in 2021 before your policy will pay anything.

The Plan F is starred because it is the only plan that covers all Medicare copays and coinsurances. It’s also important to note that as of 2020 it will no longer be available to purchase. Only those who are already enrolled may keep it. So, now is the time to capitalize on the complete coverage it provides.

Medigap Plans K & L

**For Medigap Plans K and L, after you meet your annual out-of-pocket limit and your annual Part B deductible ($203 in 2021), the Medigap plan pays 100% of covered services for the rest of that calendar year.

Medigap Plans N

***Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission. You can find this chart as well as other great info in Medicare’s Choosing a Medigap booklet as well, which you can find here.

Medicare Supplement Plans – Don’t Forget!!!

These Medicare supplement plans do not cover services like dental, glasses, transportation, hearing aids, and more. Some plans may cover these services at an extra cost or as part of a special version of the plan. If you are looking for an option that includes these additional benefits at low to no extra cost, then a Medicare Advantage plan may be a suitable option for you.Lastly, Medicare Supplement plans do not include Part D coverage. So if you choose this as your option to manage your Medicare coverage, you will need to also purchase a

What does Original Medicare cover?

What does Original Medicare cover?